You are now leaving our website and entering a third-party website over which we have no control.

Get The Most Out of My Credit Card

What is a TD Payment Plan?

Turn eligible credit card purchases into equal monthly payments over 6, 12 or 18 months - for a fee and 0% Annual Interest Rate1. Conditions apply. This convenient feature gives you more control over your budget knowing when these purchases are paid off in full. This can come in handy if you’re planning to buy a new laptop, go on a trip or start a home renovation project.

Benefits of TD Payment Plans

TD Payment Plans helps you manage your budget, while offering flexibility.

Eligibility of TD Payment Plans

Below is a breakdown to help you understand if you’re eligible. Conditions apply.

-

Personal TD credit cardholder with online or mobile banking access

-

Primary Cardholders only (Additional Cardholders are not eligible)

-

Account in good standing

-

Eligible purchase of $100 or more that has been posted to your Account3

-

Your current Account balance plus pending transactions and applicable TD Payment Plan fees cannot exceed 90% of your credit limit

-

You're a resident of a province or territory in Canada other than Quebec

-

You do not already have 25 active Payment Plans

Please login into your EasyWeb profile or the TD App to see which transactions are eligible.

Let’s break it down for you

For example, let's say you bought a $1,200 laptop and are looking to convert it into a 6, 12 or 18 month TD Payment Plan.

Setting up TD Payment Plans in EasyWeb

-

1

Sign into EasyWeb and go to your Credit Card Account Activity Page

-

2

Under ‘View Transactions’, click on 'Set up a TD Payment Plan'

-

3

Choose your TD Payment Plan

-

4

Review Terms and Conditions and click ‘Accept’ to set up your TD Payment Plan

Setting up TD Payment Plans on the TD app

- Sign into the TD app and select your credit card and tap on 'TD Payment Plans'

- Choose the eligible purchase you would like to convert into a TD Payment Plan

- Select a 6, 12, or 18 month plan and review the fee that applies

- Name your plan and confirm your email on the next screen

- Review Terms and Conditions and click 'Accept' to set up your TD Payment Plan

Frequently asked questions

Eligibility

If you’re eligible for a TD Payment Plan, you’ll see a Payment Plan offer in your account on EasyWeb or on the TD App. Your credit card account can have up to 25 active TD Payment Plans at one time.

TD Payment Plans are currently only available to residents of a province or territory in Canada other than Quebec.

Your Account balance needs to be equal to or greater than the eligible transaction amount to be eligible for a Payment Plan.

For example:

You currently have a $0 Account balance on your credit card and make a purchase of $500, the purchase would display under eligible transactions on EasyWeb or the TD App.

In a separate scenario, your credit card Account balance is $0 and you have a purchase of $500 posted to your Account. You decide to make a payment of $100 to your Account. This brings your Account balance to $400 and the purchase will not appear as an eligible transaction for a Payment Plan as your Account no longer meets the eligibility criteria. This is because your Account balance is $400 and is not equal to or greater than the $500 purchase amount.

No, not all purchases are eligible3. For a purchase to be eligible, it must be made with a personal TD Credit Card and amount to $100 or more. Purchases cannot be converted into a Payment Plan after the Payment Due Date of the statement in which the purchase first appears. Cash advances, other cash-like transactions, and service fees are also not eligible. Please check your account on EasyWeb or TD App to see if you have eligible transactions.

Business credit cards are not eligible. Purchases made on TD cards with an interest rate less than 8.99% are also not eligible.

Your credit card account can have up to 25 active TD Payment Plans at one time. However, transactions cannot be combined. If offered and accepted, each eligible transaction will be put in its own TD Payment Plan.

Yes, you can convert eligible purchases from an Additional Cardholder's credit card to a TD Payment Plan. However, only the primary cardholder can set-up a TD Payment Plan.

Plan setup and monitoring

No, a TD Payment Plan is a new feature available on eligible TD credit card purchases. Setting up a TD Payment Plan will not have any impact on your credit score, as long as you pay your minimum payment on time.

Details can be found in several places:

- In the Terms & Conditions applicable to your TD Payment Plan

- In the TD Payment Plans section of EasyWeb

- On your credit card statement each month

The fee is calculated by multiplying the full purchase transaction amount by the fee percentage. The applicable Payment Plan fee will then be added to the Payment Plan balance.

For example:

You recently purchased a $600 table, and you decide you want to convert the purchase to a 6-month Payment Plan with a total fee of 4% and a Payment Plan Annual Interest Rate of 0%.

Here’s how you would calculate the fee for your TD Payment Plan:

- Payment Plan Fee Amount = $600 X 4% = $24

The Monthly Payment Plan Amount is calculated by taking the Total Payment Plan amount (including fee) and Plan Total Interest, if any) and dividing it by the number of months for the plan.

For example:

You recently purchased a $600 table, and you decide you want to convert the purchase to a 6-month Payment Plan with a total fee of 4%.

Here’s the breakdown of your Monthly Payment Plan Amount:

- Payment Plan Fee Amount = $600 X 4% = $24

- Payment Plan balance = $624

- Monthly Payment Plan Amount (including fee) = ($600 + $24) / 6 months = $104

No, you cannot make changes to your Payment Plan terms once it is set up. However, you can close the Payment Plan through EasyWeb, if it no longer suits your needs. Once cancelled, a TD Payment Plan for that purchase cannot be reinstated, and any unpaid Payment Plan balances will become subject to your Account's annual interest rate for purchases.

No, the credit limit on your Account does not change. Only purchases made using your existing credit limit can be eligible for a Payment Plan. Amounts outstanding on your Payment Plan reduce your available credit on your account.

If you do not pay your Monthly Payment Plan Amount in full in a particular month, any unpaid portion of your Monthly Payment Plan Amount will become subject to your Account's annual interest rate for purchases beginning the first day of the Statement Period after the missed Minimum Payment.

If you do not pay your Required Payment (which is your Minimum Payment less any Monthly Payment Plan Amounts that are shown on the same statement as your Minimum Payment) by the Payment Due Date set out on your monthly Account statement in two (2) consecutive months, we have the right to close all your Payment Plans.

If you do not pay your Required Payment (which is your Minimum Payment less any Monthly Payment Plan Amounts that are shown on the same statement as your Minimum Payment) by the Payment Due Date set out on your monthly Account statement in two (2) consecutive months, we have the right to close all your Payment Plans.

If a purchase is put into a Payment Plan and you subsequently return or dispute the purchase for a refund, this will not result in the automatic closure of the Payment Plan or reduce the Monthly Payment Plan Amount. If you do wish to close a Payment Plan after returning or disputing a purchase for a refund, you may close the Payment Plan through EasyWeb.

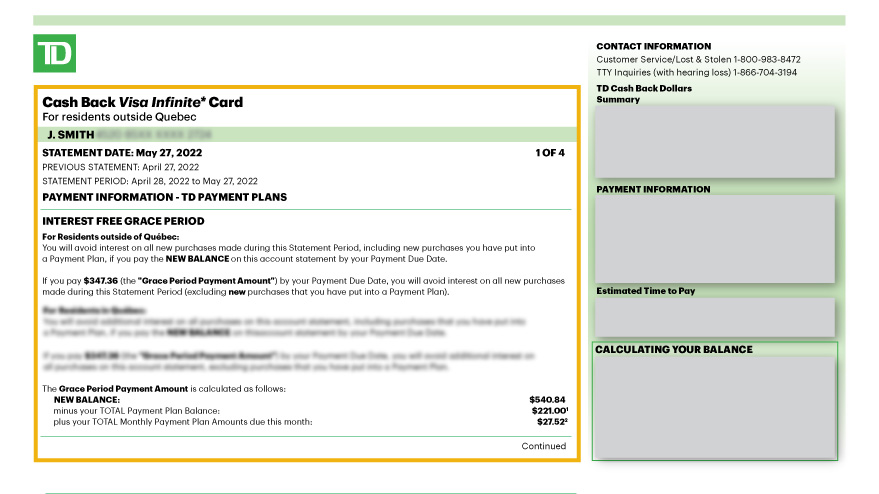

You don't have to repay your Payment Plan balance in full to take advantage of the grace period for new purchases made in a Statement Period that have not been put in a Payment Plan. Here's what you have to pay on your account by your Payment Due Date in order to avoid interest on new purchases made during a Statement Period, excluding purchases that you have put into a Payment Plan:

- The New Balance shown on your monthly statement minus your Total Payment Plans Balance(s) that are shown on that same monthly statement, plus

- Your Monthly Payment Plan Amount(s) that are due on your monthly statement.

We call this the "Grace Period Payment Amount". Starting the first statement we provide following the creation of a Payment Plan, we will show you the exact dollar amount you need to pay for each statement so you can benefit from the grace period on your Account.

- "Grace Period Payment Amount" is the amount you must pay by your Payment Due Date in order to avoid interest on new purchases made during the applicable Statement Period (excluding new purchases that have been put into a Payment Plan). The Grace Period Payment Amount for the applicable Statement Period will be shown on your Account statement starting the first statement we provide following the creation of a Payment Plan, and will be calculated as follows:

- New Balance on your monthly statement,

- minus your Total Payment Plans balance that is shown on your monthly statement,

- plus your Total Monthly Payment Plan Amount(s) that are due on your monthly statement.

- However, if you move a purchase that has already appeared on your monthly statement into a TD Payment Plan prior to the Payment Due Date of that monthly statement, the Grace Period Payment Amount will be:

- If you do not have an active Payment Plan on your current monthly statement: The New Balance shown on that monthly statement minus the purchase amount(s) converted into a Payment Plan;

- If you have active Payment Plan(s) on your current monthly statement: The Grace Period Payment Amount will be the Grace Period Payment Amount figure that is already shown on your monthly statement minus the new purchase amount(s) moved into a Payment Plan. For greater certainty, after you convert the new purchase into a new TD Payment Plan, the amount of the new TD Payment Plan will not be included in the TD Payment Plans balance that is used to calculate the Grace Period Payment Amount that is due by the Payment Due Date of that monthly statement.

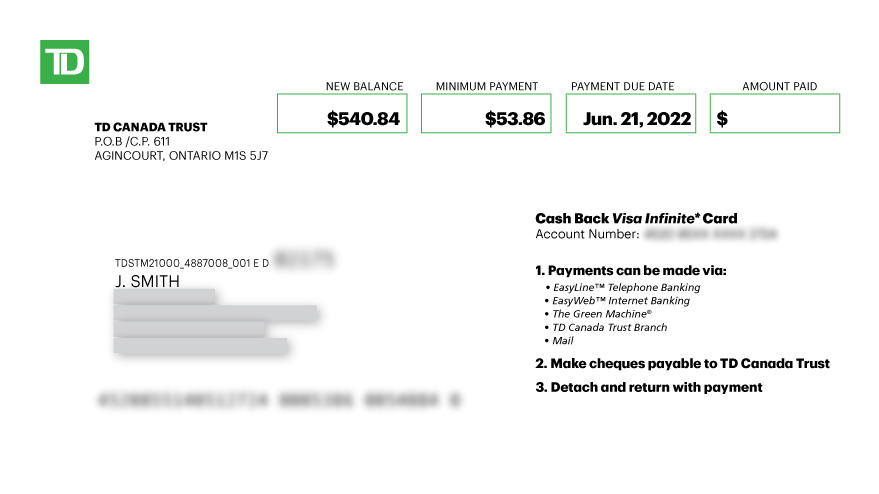

- New Balance is the total amount owing on your credit card as of the statement closing date. This will include both balances on your Account that are in a Payment Plan and balances on your Account that are not in a Payment Plan.

Minimum Payment is the amount you need to pay by the Payment Due Date.

Payment Due Date is the date your Minimum Payment is due and is shown on the Account statement.

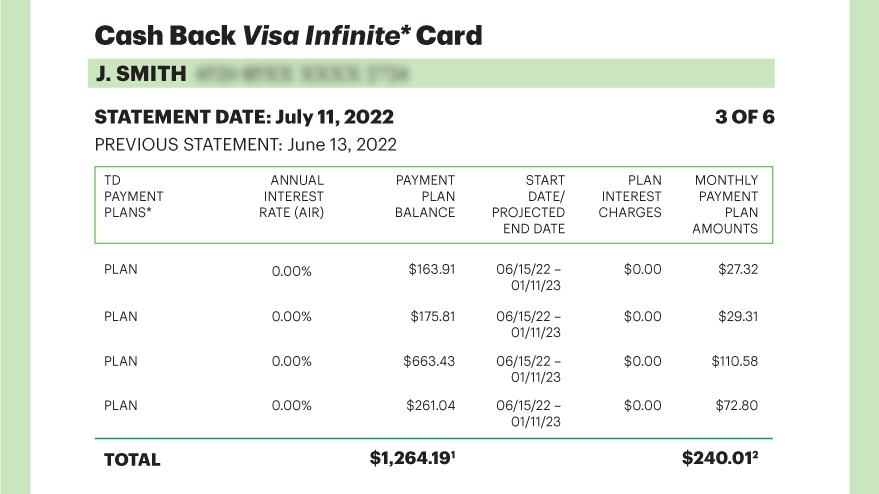

- This section appears if you have an active TD Payment Plan during the Statement Period of that Statement. It provides important information about the TD Payment Plans summarized on your Statement.

Annual Interest Rate is the interest rate applicable to the Payment Plan.

Payment Plan Balance is the outstanding balance on the TD Payment Plan as of the Statement Closing Date.

Start Date is the date the TD Payment Plan was created.

Projected End Date is the date the TD Payment Plan is set to expire.

Plan Interest Charges is the interest charged to your account for the TD Payment Plan during the Statement Period.

Monthly Plan Payment Amounts is the amount that is due to be paid on the TD Payment Plan for the Statement Period. It is included in the Minimum Payment shown at the top of your monthly statement.

Plan closure

You can close a TD Payment Plan at any time. All you need to do is log into EasyWeb, select the plan you wish to close in the Payment Plans section, and click “Close the plan”.

If your TD Payment Plans are closed, any remaining balance of the Payment Plan will become subject to your Account's then-current interest rate for Purchases.

TD has the right to close your Payment Plan if:

- You become a Resident of Quebec; or

- We do not receive your Required Payment by the Payment Due Date in 2 consecutive months; or

- You close your Account; or

- TD closes your Account or removes charging privileges for your Account or

- If you are not meeting the terms and conditions of the TD Payment Plan.

No. Once a TD Payment Plan is closed, the purchase cannot be re-enrolled.

If your TD Payment Plan is subject to a Payment Plan Fee and a Payment Plan Annual Interest Rate of 0%, and you or TD close your Payment Plan within fifty (50) days after the Payment Plan Effective Date, then TD will fully refund the applicable Payment Plan Fee. If the Payment Plan is closed after fifty (50) days, a portion of the applicable Payment Plan Fee will be refunded based on the remaining Term.

Account activity

Yes, if you have provided authorization to TD to debit your chequing or savings account to pay your Account statement's "Balance in Full" each month, we will instead debit the Grace Period Payment Amount for the applicable statement period each month until your Payment Plans expire or are closed. Please note however that if a purchase is converted into a Payment Plan after the purchase was shown on your account's monthly statement, the PAD for that statement period will continue to pay the New Balance amount that was shown on that monthly statement. This may result in your PAD paying down a partial or full amount of the new Payment Plan(s).

Refer to the TD Payment Plan Amending Agreement for more details.

If you have an account that earns rewards points, loyalty points or TD Cash Back Dollars, setting up a Payment Plan will not impact the applicable rewards terms and conditions.

Insurance coverage

If your credit card Account is enrolled in TD Credit Card Payment Protection Plan while on a Payment Plan, there are no changes and existing insurance benefits and premium calculations will continue to apply to all amounts charged to your TD credit card, including those amounts under a Payment Plan, as follows:

- Insurance Premiums

The premium calculations will remain the same and your premiums will be calculated on any amounts under your Payment Plan(s) including applicable interest on Payment Plan balances as they form part of your balance. - Insurance Benefits

The insurance benefit calculations will remain the same. However, please note that the monthly benefits may not cover your entire minimum payment in certain circumstances depending on the Payment Plan you select. You'll remain responsible for any amounts owing on your account that aren't covered by the insurance.

TD Payment Plans and Buy Now Pay Later Plans

Buy now pay later (BNPL) plans have become a popular option to allow people to spread a purchase amount over multiple smaller payments at the time a purchase is made. While this may sound similar to TD Payment Plans, these are in fact separate and distinct products with important key differences, including:

- TD Payment Plans are a feature of your credit card. As such, there is no new application or credit check required because you’re tapping into the existing credit you already have on your card.

- BNPL plans are a type of loan. They often require an application and a credit check, and any increased debt may impact your credit score.

- TD Payment Plan offers are accepted after a purchase has been made and is posted to your Account, whereas BNPL plans are initiated at the time a purchase is made, such as during online checkout.