You are now leaving our website and entering a third-party website over which we have no control.

Today's Mortgage Rates1

Explore our mortgage solutions from closed or open mortgages with fixed or variable rate options to find the right mortgage rate for you. Understanding mortgage interest rates and Annual Percentage Rate (APR) can be helpful for saving in the long term.

TD Special Mortgage Rates

TD Mortgage Prime Rate is %

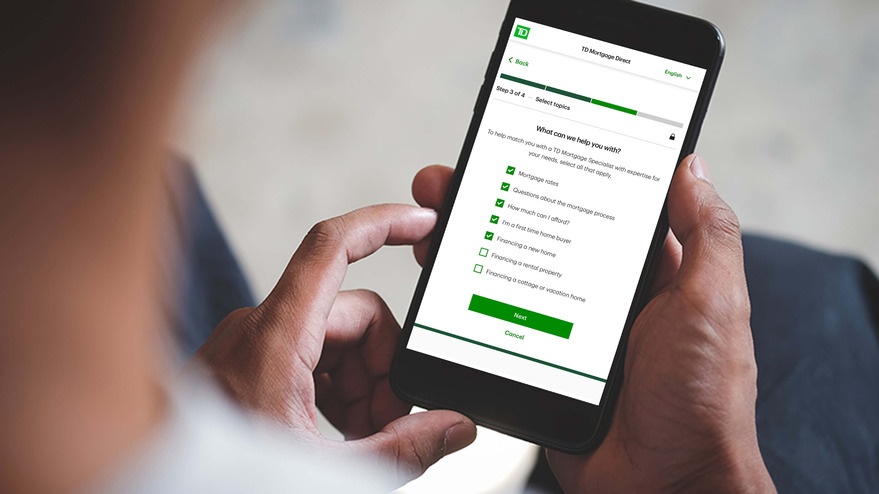

TD Mortgage Direct

Looking for tailored advice ASAP? Simply answer a few questions and TD Mortgage Direct will quickly match you with a Mortgage Specialist.

A TD Mortgage Specialist can help you:

- Understand fixed vs variable rate options and choose what works for you.

- Find a rate that works for you and switch to TD from another financial institution.

See how your mortgage rate impacts home affordability

Why get a TD Mortgage?

-

Fixed Rate Mortgages

-

Variable Rate Mortgages

-

TD Home Equity FlexLine (HELOC)

Get comfort knowing your interest rate won't increase over the term you select.

A fixed rate mortgage offers stability, and with it, peace of mind. Once you’ve selected your term, you can be assured your interest rate won't change for that period of time.

You can choose the term length: 6 month, 1, 2, 3, 4, 5, 6, 7 or 10 years.

|

Term |

Rate6 |

|---|---|

|

1 Year Open Mortgage |

|

|

1 Year Fixed Closed |

|

|

2 Year Fixed Closed |

|

|

3 Year Fixed Closed |

Posted rate: % |

|

4 Year Fixed Closed |

|

|

5 Year Fixed Closed |

Posted rate: % |

|

6 Year Fixed Closed |

|

|

7 Year Fixed Closed |

|

|

10 Year Fixed Closed |

A TD variable interest rate mortgage means the rate of interest is based on the TD Mortgage Prime Rate, which can go up and down over the term of a mortgage loan.

|

Term |

Rate |

|---|---|

|

5 Year Variable Closed Mortgage |

Posted Rate: Special Rate 2: % (TD Mortgage Prime Rate % %) |

|

5 Year Variable Open Mortgage |

A HELOC is an alternative to a mortgage. You get the option to borrow only what you need, as you need it. Plus, as it is secured by your real estate, you may get the benefit of an interest rate that is lower when compared to unsecured credit interest rates.

TD Home Equity FlexLine is a way to use your most powerful borrowing tool – your home. As you pay back the amount you owe, the amount of credit available to you increases until it reaches your credit limit. It’s available when you need it, through a variety of convenient options, 24/79.

Mortgage interest rates FAQs

Annual Percentage Rate (APR) is the cost of borrowing expressed as a percentage. It includes interest and applicable fees (for example property valuation fees). The APR is not the rate used to calculate your regular payments.

A fixed interest rate means your interest rate, along with your principal and interest payments, will stay exactly the same during your mortgage term.

With a variable interest rate, your interest rate can fluctuate based on changes in our TD Mortgage Prime Rate. While your payments will remain the same, the amounts from each payment that go toward the principal and interest can vary10.

It's important to take a closer look at the differences between fixed and variable interest rates before you make a decision.

A mortgage rate hold is the locking in of a specified mortgage rate for a set period of time. This only applies to fixed rate mortgages, since the interest rate of variable rate mortgages can fluctuate.

Once you have a TD Mortgage Pre-Approval, you get a 120-day rate hold which holds the interest rate on your pre-approval term for up to 120 days subject to all the conditions, even if interest rates go up.

Related articles

Other ways to connect

Find a rate that works for you

Find a rate that works for you